Corteva: Strong Seed segment performance more than offset Crop Protection headwinds in 1H

- Strong Seed segment performance more than offset Crop Protection headwinds in 1H

- Full Year forecast3 reflects continued growth in Revenue, Operating EBITDA1 and Margin1

- Executing well, on-track to deliver 2025 financial growth targets

- Increased dividend 7% on an annualized basis, effective in the third quarter

05 August 2023, US: Corteva, Inc. (NYSE: CTVA) (“Corteva” or the “Company”) reported financial results for the second quarter and six months ended June 30, 2023.

First Half 2023 Highlights

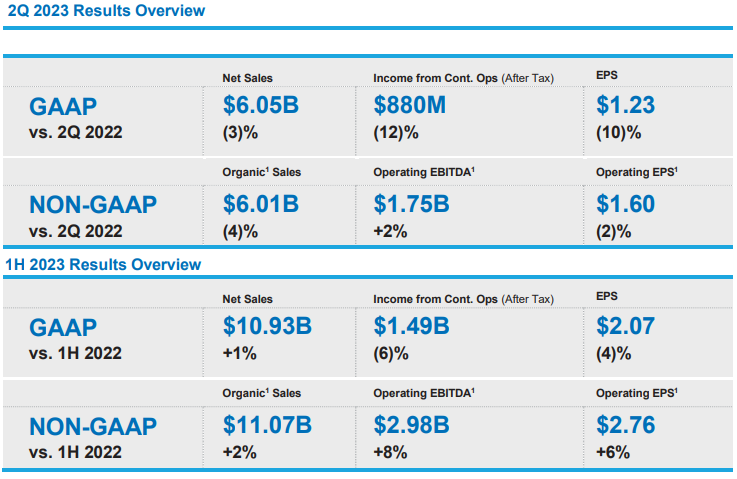

- First half 2023 net sales rose 1% versus prior year led by the Seed segment. Organic1 sales increased 2% in the same period with gains in North America2 and EMEA2.

- Seed net sales grew 8% and organic1 sales increased 9%. Price was up 14% globally, led by continued execution on the Company’s price for value strategy and recovery of higher input costs. Volume declines were driven by the exit from Russia, lower corn planted area in EMEA2, and lower Safrinha volumes in Latin America, partially offset by increased corn acres in North America2.

- Crop Protection net sales and organic1 sales both decreased 9%. Volume declines were driven by strategic product exits, inventory destocking, and timing of seasonal demand due to weather and delayed farmer purchases. Price gains reflected pricing for value and strong execution in response to cost inflation led by EMEA2 and North America2.

- GAAP income and earnings per share (EPS) from continuing operations were $1.49 billion and $2.07 per share for the first half of 2023, respectively, with declines versus prior year driven by lower volumes, unfavorable currency and non-cash charges associated with legacy retirement plans. Operating EBITDA1 was $2.98 billion, an 8% improvement over prior year on price execution and productivity actions, partially offset by lower volumes coupled with cost and currency headwinds. Operating EPS1 was $2.76 per share, up 6% compared to prior year.

- Management revised full year 2023 net sales and earnings guidance3. Net sales is expected to be in the range of $17.9 billion to $18.2 billion and Operating EBITDA1 is expected to be in the range of $3.50 billion to $3.65 billion. Operating EPS1 is expected to be in the range of $2.75 to $2.90 per share.

“Corteva once again delivered growth in the first half of 2023, driven by its diversified and unique technology portfolio providing further evidence that our strategy is creating significant value.

“The Seed business had another terrific quarter which reflects the strong demand for our superior technology: today, Enlist E3™ is the number one selling soybean technology in the U.S. The Crop Protection business demonstrated resilience and margin expansion, despite headwinds from industry-wide inventory destocking, as the team continued to better position the portfolio and reduce cost.

“As we look to the second half, demand fundamentals remain positive: farmer net incomes remain above historical averages and they continue to focus on technology for both yield enhancement and preservation. At Corteva, we will continue to focus on our key controllables: delivering best in class solutions and technologies to farmers, proactively managing our cost structure, while increasing investments in innovation for the future,” said Chuck Magro, Corteva Chief Executive Officer.

Company Updates

- Enlist E3™4 Becomes Number One Selling Soybean Technology in the U.S.

- The Company expects 2023 Enlist E3™4 U.S. market penetration of at least 55%, representing ~75% of Corteva’s lineup – a notable accomplishment considering this technology has only been in the market for 4 seasons. The percentage of Enlist E3™4 with proprietary Corteva germplasm is expected to exceed 80%.

- Recent Product Announcements Illustrate Value of Differentiated Innovation Pipeline

- The Company announced that PowerCore® Enlist® Refuge Advanced® (RA) corn will be available for planting in the 2024 growing season in the U.S. and Canada. Farmers will have the added flexibility of integrated refuge, along with an advanced combination of above-ground pest control, herbicide tolerance and industry-leading genetics with PowerCore® Enlist® RA corn.

- The Company also announced Bexoveld™ active as the brand name for the newest herbicide from its robust innovation pipeline. The active ingredient will offer cereal farmers another tool for controlling broadleaf weeds. Bexoveld™ active is a new proprietary molecule discovered by Corteva and is a third-generation 6-Arylpicolinate (6-AP) herbicide built upon the Company’s deep knowledge of Arylex™ active and Rinskor™ active herbicides. Corteva expects to launch Bexoveld™ active in North America in 2028 and in Europe in 2030, pending regulatory reviews.

- Recent Biologicals Announcements Reinforce Leading Market Position in Growing Segment

- The Company entered into an exclusive agreement with BioCeres to accelerate the regulatory processes required to bring a cutting-edge bioinsecticide to the European market. The product is an extremely viable biological insecticide that can be as effective as conventional insecticides, with target crops including corn and other cereals, as well as sunflower and rape seeds.

- The Company entered into a licensing agreement with Lavie Bio, which grants Corteva exclusive rights to further develop and commercialize bio-fungicides targeting fruit rots and powdery mildew. This collaboration demonstrates both companies’ commitment to providing farmers with environmentally friendly, sustainable tools with proven effectiveness.

- The Company announced that Utrisha™ N, a microbe-based nitrogen fixation product, has been verified as a United States Department of Agriculture (USDA) Process Verified Program – the first biostimulant to be included in the Program. The USDA Process Verified shield assures farmers that the USDA validated quality management systems and specific process points Corteva established to indicate the quality of Utrisha™ N.

Summary of Second Quarter 2023

For the second quarter ended June 30, 2023, net sales decreased 3% versus the same period last year. Organic1 sales declined 4%.

Volume declined 13% versus the prior-year period driven by strategic product exits and inventory destocking in the Crop Protection segment. Lower Seed volumes were driven by lower corn planted area in EMEA and the exit from Russia, partially offset by increased corn acres in North America.

Price increased 9% versus prior year, reflecting continued execution on the Company’s price for value strategy and recovery of higher input costs.

GAAP income from continuing operations after income taxes was $880 million in second quarter 2023 compared to $1.0 billion in second quarter 2022. Operating EBITDA1 for the second quarter was $1.75 billion, up 2% compared to prior year, translating into approximately 140 basis points of margin improvement.

Seed Summary

Seed net sales were $4.3 billion in the second quarter of 2023, up from approximately $3.9 billion in the second quarter of 2022. The sales increase was driven by a 12% increase in price and 1% favorable impact from portfolio, partially offset by a 3% decline in volume and a 2% unfavorable currency impact.

The increase in price was driven by strong demand for top technology products, and strong operational execution, with global corn and soybean prices up 14% and 8%, respectively. Lower volumes were driven by reduced corn planted area in EMEA, fewer soybean acres in North America, and the 2022 decision to exit Russia, partially offset by increased corn acres in North America. Unfavorable currency impacts were led by the Canadian Dollar and the Turkish Lira.

Segment operating EBITDA was $1.5 billion in the second quarter of 2023, up 18% from the second quarter of 2022. Price execution, reduction of net royalty expense, and ongoing cost and productivity actions more than offset higher input and freight costs, lower volumes, and the unfavorable impact of currency. Segment operating EBITDA margin improved by approximately 280 basis points versus the prior-year period.

Seed net sales were $7.0 billion in the first half of 2023, up from approximately $6.5 billion in the first half of 2022. The sales increase was driven by a 14% increase in price and 2% favorable impact from portfolio. This gain was partially offset by a 5% decline in volume and a 3% unfavorable currency impact.

The increase in price was driven by strong demand for top technology and operational execution globally, with global corn and soybean prices up 15% and 7%, respectively. Pricing actions more than offset currency impacts in EMEA. The decline in volume was driven by the 2022 decision to exit Russia, lower corn planted area in EMEA, and lower Safrinha volumes in Latin America, partially offset by increased corn acres in North America. Unfavorable currency impacts were led by the Turkish Lira and the Canadian Dollar.

Segment operating EBITDA was $2.1 billion in the first half of 2023, up 17% from the first half of 2022. Price execution, reduction of net royalty expense, and ongoing cost and productivity actions more than offset higher input and freight costs, the unfavorable impact of currency, and lower volumes. Segment operating EBITDA margin improved by approximately 240 basis points versus the prior-year period.

Crop Protection Summary

Crop Protection net sales were approximately $1.8 billion in the second quarter of 2023 compared to approximately $2.3 billion in the second quarter of 2022. The sales decrease was driven by a 29% decrease in volume and a 1% unfavorable impact from currency, partially offset by a 4% favorable impact from portfolio and a 3% increase in price.

The decrease in volume was driven by strategic product exits, inventory destocking trends impacting volumes across all regions, and timing of seasonal demand due to weather and delayed farmer purchases. The portfolio impact was driven by the Biologicals acquisitions. The increase in price was broad-based, with gains in most regions led by EMEA, and mostly reflected pricing for the value of our differentiated technology, including pricing for new products.

Segment operating EBITDA was $320 million in the second quarter of 2023, down 37% from the second quarter of 2022. Volume declines, higher input costs, and increased R&D investment more than offset pricing and productivity actions. Segment operating EBITDA margin declined by approximately 410 basis points versus the prior-year period.

Crop Protection net sales were approximately $4.0 billion in the first half of 2023 compared to approximately $4.4 billion in the first half of 2022. The sales decrease was driven by a 16% decrease in volume and a 3% unfavorable impact from currency. These declines were partially offset by a 7% increase in price and a 3% favorable portfolio impact.

The decrease in volume was driven by strategic product exits, inventory destocking trends impacting volumes across all regions, and timing of seasonal demand due to weather and delayed farmer purchases.

The increase in price was broad-based, with gains in most regions led by EMEA and North America, and mostly reflected pricing for the value of our differentiated technology, including pricing for new products, and currency in EMEA. Unfavorable currency impacts were led by the Turkish Lira and Chinese Renminbi. The portfolio impact was driven by the Biologicals acquisitions.

Segment operating EBITDA was $923 million in the first half of 2023, down 8% from the first half of 2022. Pricing execution and productivity actions were more than offset by lower volumes, higher input costs, and the unfavorable impact of currency. Segment operating EBITDA margin increased by more than 40 basis points versus the prior-year period largely driven by pricing execution and productivity actions.

2023 Guidance

The outlook for agriculture remains overall positive in 2023, with high demand for grain and oilseeds. Commodity prices are above historical averages, and farm balance sheets and income levels remain healthy, leading growers to prioritize technology to maximize return. Crop Protection order patterns are being influenced by product availability, higher interest rates, and a deferral of purchases until closer to usage, leading to an update to full-year 2023 net sales and earnings expectations.

The Company updated its previously provided guidance3 for the full-year 2023 – lowering sales and earnings expectations for this period. Corteva expects net sales in the range of $17.9 billion to $18.2 billion, growth of 3% at the mid-point. Operating EBITDA1 is expected to be in the range of $3.50 billion to $3.65 billion, growth of 11% at the mid-point. Operating EPS1 is expected to be in the range of $2.75 to $2.90 per share, growth of 6% at the mid-point.

The Company is not able to reconcile its forward-looking non-GAAP financial measures to its most comparable U.S. GAAP financial measures, as it is unable to predict with reasonable certainty items outside of its control, such as Significant Items, without unreasonable effort.

Also Read: The rise of India’s population and the rise of the technologies to feed it

(For Latest Agriculture News & Updates, follow Krishak Jagat on Google News)