Essential fertilizers ride the coronavirus storm

Guest Author: Julia Meehan, Managing Editor, Fertilizers, ICIS

26th June 2020, London: The domino effect of the coronavirus, as it has spread across the globe, has so far had a limited impact on the fertilizer industry. However, the full effects of the global pandemic are starting to show in some sectors owing to cashflow problems caused by decomposing crops, such as fruit and vegetables.

China, having been the epicentre of the pandemic, is starting to get back to normal and production rates have increased for all fertilizers. The nation is the largest fertilizer consumer in the world, on average consuming close to 50m tonnes/year. It is also a key exporter of urea.

When lockdown began in China, the impact was huge in terms of cuts in production owing to a shortage of labour. Problems with transportation, by both rail, road and sea, also had a big impact up and down the fertilizer chain resulting in stock piling up.

The biggest impact for China was on phosphoric acid which is used to produce phosphate. Fertilizer facilities in Hubei province account for up to a third of the country’s total capacity. Because of this, China turned from the largest exporter of diammonium phosphate (DAP) to a net importer.

But as China started to ease its way out of lockdown, the flow of all fertilizers has recovered very quickly and life is getting back to normal again.

Urea was less impacted in China with Hubei province only accounting for around 3% over China’s total capacity.

As the pandemic spread across nations, many countries started to feel the full impact of the deadly virus at a time when fertilizer application was at a seasonal high, particularly for the northern hemisphere.

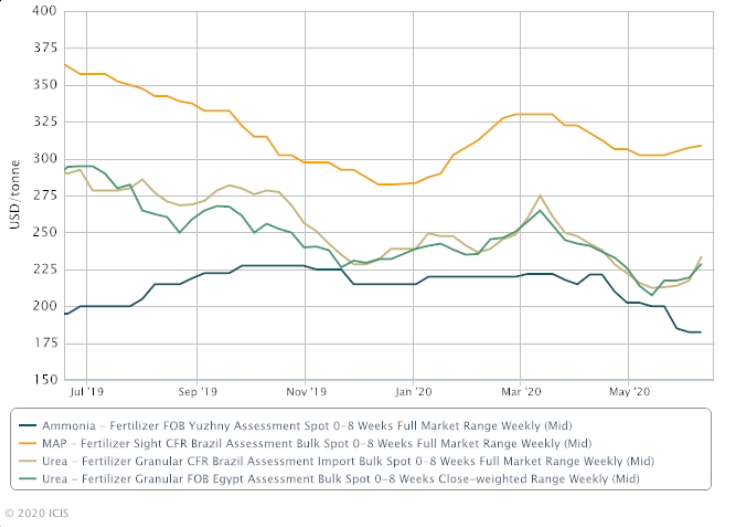

Indeed, during March, demand for all fertilizers was healthy and the value of feedstocks and nutrients held steady and in some instances firmed.

There was pressure on pricing in April-May but the fertilizer sector most certainly did not experience the sharp and dramatic price falls seen in related markets such as gas, oil and petrochemicals.

In June, sentiment has turned and most fertilizer prices have increased.

As the virus took hold as it moved across the global, agricultural and industrial sectors learned lessons from China and many were given government support. The transportation of fertilizers across European boarders continued but with strict measures in place to protect truck drivers and the workforce.

France, which is the largest fertilizer user in Europe, moved through the months of Spring with largely no impact on supply or demand, although some cracks are starting to appear now. Cash flow problems are emerging for some farmers and the wet start to 2020, following by a dry April and May, has damaged crops.

Germany too has seen crops rotting, largely because of the coronavirus. The closure of cafes, bar and restaurants which consume large quantities of French fries has led to a 60% drop in demand for potatoes, for example.

Similar to Europe, the pandemic is now raging across Latin America just as the fertilizer season gets into full swing. Demand in the past weeks has been healthy for Latin America, with large volumes of fertilizer moving to Brazil and Argentina.

The fertilizer sector has fared better during the global pandemic, compared to the petrochemical and energy sectors, in terms of production. Fertilizer makers have benefited from cheap feed and energy costs meaning that even marginal producers have continued to operate, and the markets have not felt any shortness of availability.

There has been some concern about new capacities due to come on stream in 2020 creating oversupply. Some of these projects are likely to be delayed or pushed back to 2021 because of the fact that the health and safety of workers is paramount.

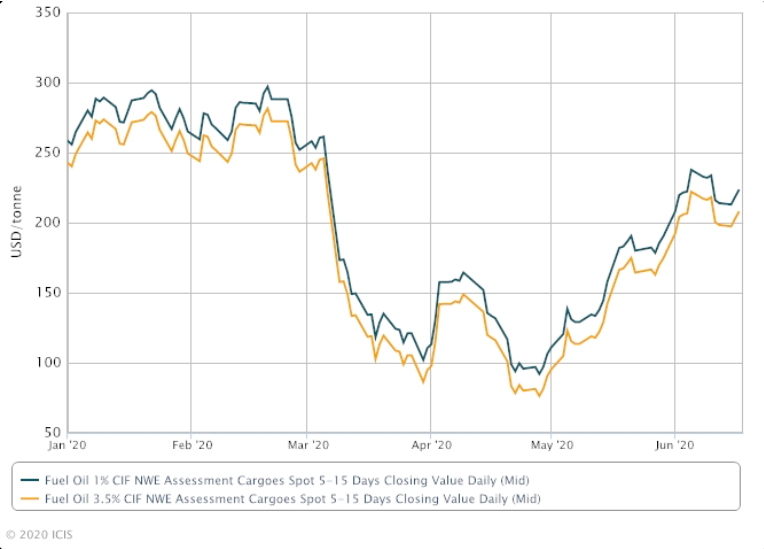

Discussions about the impact of IMO 2020 and Brexit on the fertilizer market have been virtually wiped out by the coronavirus and its impact, or rather lack of, so far into the pandemic.

The potential for a sharp rise in bunker fuel prices because of IMO 2020 regulations has not been realised because of the dramatic fall in fuel oil costs.

There appears to have been be no serious demand destruction across the fertilizer sector since the first case of the virus outside China was confirmed on 13 January 2020. For many producers, cooperatives, wholesalers and farmers it has been business as usual.

But the outlook remains uncertain, with much talk and concern about of a second wave and what this might mean to already broken economies.

Currency fluctuations, political unrest and huge levels of unemployment in both developed and developing nations will inevitably have an impact in the months and years ahead.

Regardless of all of these factors, the world still needs feeding. And considering that up to 50% of the food we eat would not be available without fertilizers, this is an industry that will remain robust and continue to be deemed essential.